Autodesk investigates: A whistleblower raises issues but there's no restatement

Autodesk investigates: A whistleblower raises issues but there's no restatement

Seems like tailor-made accounting ripe for SEC, and DOJ, scrutiny.

This is a cross-post with my frequent collaborator, Olga Usvyatsky, of a report we co-authored on her site, Deep Quarry.

On May 31, 2024, Autodesk (Ticker: ADSK) reported the results of an internal investigation of its free cash flow and non-GAAP operating margin practices. The company had announced on April 1 that it would be filing its 10-K late because after its earnings release on February 29, 2024, “information was brought to the attention of management, which promptly informed the Audit Committee of the Board of Directors of the Company”.

While the investigation did not result in a restatement of previously reported results, Autodesk admitted that it had shifted certain charges and collections from one period to another to influence its free cash flow and operating margin metrics.

In its delayed annual report, filed on June 10, 2024, Autodesk warned that the regulators could further scrutinize the findings of the internal investigation:

In early March 2024, the Audit Committee of Autodesk’s Board of Directors commenced an internal investigation with the assistance of outside counsel and advisors regarding the Company’s free cash flow and non-GAAP operating margin practices (the “Internal Investigation”). On March 8, 2024, the Company voluntarily contacted the U.S. Securities and Exchange Commission (“SEC”) to inform it of the Internal Investigation.

On April 3, 2024, the United States Attorney’s Office for the Northern District of California (“USAO”) contacted the Company regarding the Internal Investigation. The Company voluntarily provided the SEC and USAO with certain documents relating to the Internal Investigation and will continue to cooperate with the SEC and USAO. At this stage, the Company cannot reasonably estimate the amount of any possible financial loss that could result from this matter.

Incentivizing customers to pay upfront for multiyear agreements is a valid working capital management tool, and Autodesk says previously filed financial statements were not misstated. So why do we think the SEC and Department of Justice may pursue the case?

Based on the language used by Autodesk to describe the Audit Committee’s findings, its multiyear billing practices were used to meet free cash flow (FCF) and operating margin targets. In addition, the remedial measures proposed by the Audit Committee — including reviewing processes around “financial communications and disclosures” — suggest that Autodesk failed to provide appropriate disclosure to the general public. (Note, however, that Autodesk did not report internal control or disclosure control weaknesses.)

As Francine McKenna explained in The Dig piece, recent SEC enforcement actions are more likely to cite disclosure violations than to bring accounting fraud charges under Section 10b-5 of the 1933 Securities Act:

The Securities and Exchange Commission has been settling cases where companies and executives manipulate financial results to meet analyst expectations or internal metrics using Section 17(a) of the 1933 Securities Act more often than 10b and 10b-5. The cases the SEC brought after the financial crisis were charged predominantly under Section 17(a).

Historically, Autodesk billed customers upfront for multiyear contracts, accelerating the cash collection to the earlier years of the contract. In 2022, it announced it had started shifting the billing cycle for multiyear enterprise contracts to annual. However, in practice, it continued to bill certain enterprise customers upfront.

The excerpt below is from the explanatory note of the 10-K filing dated June 10, 2024 (emphasis added):

The Company has historically relied on multiyear contracts with its enterprise and product subscription customers, billed upfront, to help meet its free cash flow targets. During the relevant period, the Company engaged in programs designed to incentivize customers to accept multiyear upfront billing, renew early, and/or pay before the end of the fiscal year.

The Company has disclosed its practice of incentivizing customers to adopt multiyear upfront billing arrangements. It has also acknowledged that discounted multiyear upfront contracts reduce revenue and lower billings in out years. Though prior to fiscal year 2024, the Company did not quantify free cash flow attributable to multiyear upfront billings, it has noted the contribution of upfront collections to fluctuations in the Company’s quarterly reported long-term deferred revenue.

During fiscal year 2022, the company announced that it had begun to shift enterprise customers to contracts billed annually, and that it had assumed fiscal 2023 enterprise contracts would be billed annually. The company subsequently determined, however, to pursue multiyear upfront contracts with enterprise customers to help meet its fiscal year 2023 free cash flow goal. Upfront billings of enterprise customers in fiscal year 2023 substantially exceeded historical levels, helping the company to meet its lowered annual free cash flow target.

In addition, during the relevant period, certain decisions regarding discretionary spending, collections, and accounts payable were informed by their anticipated effects on the company's external free cash flow and/or non-GAAP operating margin targets. The resulting actions generally served to reduce reported free cash flow and/or lower reported margin in the current period. Though free cash flow was one factor in the company's executive compensation program, these decisions were not calculated to influence compensation outcomes.

According to Autodesk, the decision to continue billing enterprise customers upfront helped meet its free cash flow targets, an important non-GAAP metric analysts use to gauge liquidity. Autodesk’s actual free cash flow for the year ending January 31, 2023 (fiscal 2023) was $2.031 billion compared to the guidance of $2 billion to $2.08 billion. Missing the target, which was already reduced from the $2.13 to $2.21 billion range initially reported in Q4 2022, would have likely hurt the share price.

Yet, the 2023 free cash flow improvement came at the expense of a softer 2024 guidance, which fell short of the market estimates and led to a double-digit stock price drop. According to analysts interviewed by MarketWatch, the shift to annual billings is to blame:

Citi Research analyst Tyler Radke, who has a buy rating and a $265 target price, said the company’s shift to annual billings from multiyear contracts dragged on free cash flow, and said “management applied a more reasonable set of conservatism vs. prior guides,” when it came to the outlook.

The impact to free cash flow figured heavily in other notes. Autodesk forecast $1.15 billion to $1.25 billion free cash flow for the year, while Wall Street, on average, had been expecting $1.31 billion….

…MoffetNathanson analyst Sterling Auty, who has an underperform rating and a $203 price target on Autodesk, said the “shift to annual billings is having an even larger impact on free cash flow for fiscal 2024 than what our estimates, and the Street, had anticipated after the preliminary outlook was given a quarter ago.

Autodesk emphasized in the 10-K Explanatory note that it had previously disclosed both the practice of incentivizing customers to pay upfront and the impact of such a practice on cash flow volatility. However, by Autodesk’s own admission, the impact prior to 2024 was not quantified.

Arguably, the overall impression from Autodesk’s communication in fiscal 2023 was that it is winding down the practice of upfront billings. For instance, during the November 22, 2022, conference call (fiscal Q3 2023), it noted that it wants to transition “…as fast as possible because we really like to get this financial noise behind us.” In practice, however, the 2023 upfront multiyear billings “…substantially exceeded historical levels”.

Understanding the extent of 2023 billings was likely material to modeling the 2024 cash flow levels. Omitting material information could lead to overoptimistic expectations about future FCF, misleading investors, and exposing Autodesk to shareholders’ litigation and regulatory scrutiny.

Historical perspective – lessons from SEC enforcement action against Under Armour and General Electric Co (GE)

In our opinion, several characteristics of Autodesk’s disclosure deficiencies appear to be conceptually similar to the disclosure deficiencies cited by the SEC in recent enforcement actions.

The SEC fined Under Armour (Ticker: UAA) $9 million on May 3, 2021, for misleading investors about its future revenue growth. The SEC’s order found that Under Armour accelerated (“pulled forward”) existing shipments to meet its revenue projections and failed to disclose to investors its reliance on the pulled forward shipments:

…Under Armour misleadingly attributed its revenue growth during this period to various factors without disclosing to investors material information about the impacts of its pull forward practices. The order finds that Under Armour failed to disclose that its increasing reliance on pull forwards raised significant uncertainty as to whether the company would meet its revenue guidance in future quarters. According to the order, using these undisclosed pull forwards, Under Armour was able to meet analysts' revenue estimates.

Let’s compare and contrast the cases.

Both Autodesk and Under Armour used business practices that improved the current period’s results by sacrificing future performance;

In both cases, aggressive business practices were used to meet targets and estimates for important financial metrics;

Both companies allegedly omitted material disclosure related to the impact of aggressive business practices on future periods.

I highly recommend reading The Dig piece for additional examples and an in-depth analysis of why disclosure-related enforcement actions are lately more prevalent than scienter-based accounting fraud cases.

The Dig also discussed SEC enforcement action against General Electric Co (GE) in a separate piece.

According to the SEC order, GE agreed to pay $200 million to settle charges related to disclosure violations related to its power and insurance divisions. The charges, among others, included failure to disclose the impact of factoring intercompany receivables on one ofGE’s key non-GAAP metrics, Industrial Cash Flow (emphasis added):

Selling longer term receivables to GE Capital allowed GE immediately to report increased industrial cash flow, without disclosing that GE was depleting future cash flows by moving them into the present. As a result of this new practice, called “deferred monetization,” GE boosted a publicly reported cash flow measure by more than $1.4 billion in 2016 and more than $500 million in the first three quarters of 2017. GE failed to disclose to investors its adoption and reliance on deferred monetization which increased present industrial cash flow at the expense of future years.

It looks familiar, right? While GE tapped intercompany receivables (vs. external billings) to boost the cash flow metric, conceptually, we see the same pattern over and over—companies are using aggressive, undisclosed business practices to achieve short-term performance goals by pulling revenue or cash flow forward.

Arguably, liquidity measurements such as free cash flow have received limited scrutiny from the regulators so far. Our search in the Audit Analytics AAER database identified only two cases in the past decade that involved false and misleading statements related to disclosure of the cash flow metrics — namely, the enforcement action against GE in December 2020 discussed above and an enforcement action against StoneMor Partners L.P. in December 2019.

SEC comment letters – routine reviews of SEC’s Division of Corporation Finance – are more common. Based on an analysis, roughly 100 companies received SEC comments related to FCF disclosure in the past five years.

Autodesk and Chemours: Two disclosed cases of cash flow manipulation in six months. Is it a coincidence?

In the past six months, at least two public companies — Autodesk and Chemours Co (Ticker: CC) — initiated internal investigations related to pulled-forward cash flow. In both cases, cash flow metrics were also used for executive compensation purposes, and both companies disclosed regulatory probes.

Is it a coincidence or the beginning of a troubling trend of misleading disclosures? Challenging macroeconomic conditions and a prolonged high interest rate environment put the focus on liquidity and, therefore, pressure companies to manage working capital more efficiently. Tying executive compensation to hard-to-achieve cash flow metrics is a double-edged sword. While it aligns managerial interests with those of the shareholders, it may also create an incentive to manipulate the metrics.

There's a deluge of news about accounting: ADM, Chemours, Caterpillar, Autonomy, and Evergrande

Of course, the devil is in the details. Based on Autodesk's language, an inadvertent communication failure caused the allegedly misleading disclosure. According to Autodesk, executive compensation considerations did not influence the decision to manipulate the cash flow.

Yet, based on Chemours' disclosure, management manipulated the timing of the payments and collections and concealed the cash flow manipulation from the Board of Directors, prompting Chemours to put the CEO, CFO, and Controller on administrative leave. Putting top executives on administrative leave is an indication that the issues are serious.

From Chemours’ 10-K filing:

the Company's then-Chief Executive Officer, then-Chief Financial Officer, and then-Controller, placed on administrative leave on February 28, 2024, engaged in efforts in the fourth quarter of 2023 to delay payments to certain vendors that were originally due to be paid in the fourth quarter of 2023 until the first quarter of 2024, and to accelerate the collection of receivables into the fourth quarter of 2023 that were originally not due to be received until the first quarter of 2024;

these individuals engaged in these efforts in part to meet free cash flow targets that the Company had communicated publicly, and which also would be part of a key metric for determining incentive compensation applicable to executive officers;

there was a lack of transparency with the Company’s Board of Directors by the members of former senior management who were placed on administrative leave with respect to these actions.

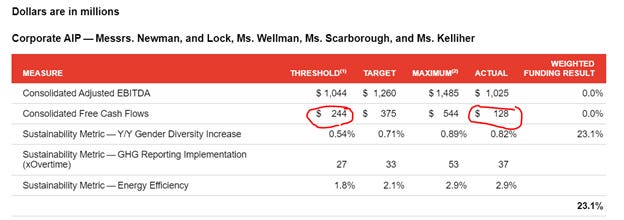

For Chemours, 42.5% of the annual incentive plan was tied to meeting the minimal free cash flow threshold of $244 million (page 47 of the proxy):

Note that the actual $128 million FCF used for compensation purposes was adjusted to take into consideration “timing actions” – a euphemism used by Chemours to describe the working capital manipulation:

The Corporate AIP results reflect the calculation of Free Cash Flows after taking into account the net impact of the working capital timing actions and the business segment results reflect the impact of the respective working capital timing actions as applicable to each particular segment. This calculation reduced the payout for incentive compensation tied to Free Cash Flow to $0 for all NEOs.

The CLDC and the Board further applied full negative discretion to determine that Mr. Newman and Mr. Lock would receive no 2023 AIP awards.

Note also that the Board used its discretion to forfeit all awards for the CEO and CFO under the 2023 Annual Incentive Plan (AIP).

Let’s pause and think - why would a company voluntarily hold back part of the compensation? Among other reasons, to signal to investors and regulators that the company discourages bad behavior and takes the issues seriously.

Director of Division of Enforcement, Gurbir Grewal, outlined in his May 23, 2024, speech five principles of effective cooperation with SEC investigations. According to Grewal, in certain cases clawing back compensation is an essential step in a remediation process (emphasis added):

Principle three: don’t stop with the self-report. Remediate. Effective remediation can further underscore a firm’s commitment to compliance and help them build a case for cooperation credit.

Depending on the circumstances of the conduct at issue, remediation can take many forms. But there are certain remedial measures that are applicable to any number of situations. They include disciplining or dismissing the actors responsible for the violations; strengthening relevant internal controls and policies and procedures; conducting training – or re-training – on the conduct at issue; hiring personnel with relevant expertise; clawing back or recovering certain executive compensation; and repaying harmed investors.

We recently alerted our readers that another company - namely, Under Armour that was fined $9 million by the SEC in 2021 for a failure to disclose reliance on pulled forward revenue - decided to forfeit part of the executive compensation after correcting immaterial accounting errors. The forfeiture was voluntary because the new SEC clawback rule that requires companies to recover erroneously paid compensation after restatements would not apply to Under Armour until the next year.

Here is what we observed - the full article is available to paid subscribers:

The 10-K language describing the errors does not indicate that the financials were intentionally manipulated or that the management knew about the errors and left them uncorrected. However, the pattern of accounting-related issues could arguably raise concerns about executives benefiting from (albeit unintentional) errors and correcting them just before the new clawback rule kicked in. Voluntary compensation forfeiture may alleviate those concerns and signal the willingness of the management to rectify the issues.

Conclusion

It is important to remember that not all investigations end with an enforcement action. A recently published academic paper finds that only about a quarter of SEC investigations lead to enforcement action, and the remaining cases are closed without finding any wrongdoing (Solomon and Soltes, Journal of Empirical Legal Studies, 2021).

However, even probes that do not result in a formal enforcement action are disruptive and could be detrimental to the share price because of lost investors' confidence and the negative effect of the legal costs on the bottom line. As a general rule, investors should also be mindful that legal reserves are often understated because the timing and extent of legal settlements are hard to predict.

© Francine McKenna, The Digging Company LLC, 2024