Crosspost: Despite the name, companies use accounting tactics that assign a lot of certainty to UTPs

Companies disclose little, reserve less, and often bet big on prevailing in material tax disputes over uncertain tax positions. Auditors feign concern, but investors deserve to know more.

This is a cross-post with Deep Quarry, the newsletter I occasionally collaborate on with Olga Usvyatsky. If you value our work, please subscribe!

The PwC accounting guide defines uncertain tax positions (UTP) as “tax positions taken that are subject to varied interpretations of applicable tax law.” Accounting rules require companies to record a tax liability for an uncertain tax position if there is a more-likely-than-not probability — usually interpreted as a more than 50% likelihood — that the position will stand if challenged in a court.

As Olga Usvyatsky discussed with the Financial Times, if a company overestimates its chances to prevail in court, shareholders may face a sharp hit to net income:

“The question is, do companies correctly estimate the probabilities?,” says accounting researcher Olga Usvyatsky. “If they don’t, then investors are in for a big surprise, in some cases a multibillion-dollar surprise.”

To make an uncertain tax positions analysis even more intriguing, several companies, including prominent names such as Coca-Cola and Uber, are paying deposits or the full amount due in order to appeal tax disputes, then recording the payment as a receivable, an asset or IOU from the tax authority, despite having no guarantee of recovery. This accounting practice, which counts on paid-for legal opinions that appeals have a high probability of being successful, allows companies to avoid an immediate hit to profit for payments that were not previously reserved and expensed. Instead, companies treat the payments as IOUs from tax authorities and as non-current assets because the appeals often take years. These tax receivables may also generate non-cash, accrued interest income, further flattering earnings. That's despite the fact the cash refund plus interest might never be received.

While treating deposits and full payments to settle a tax dispute as an asset may seem counterintuitive, this accounting treatment is compliant with GAAP. PwC —Uber's auditor and tax advisor — publishes accounting guidance that provides an example of a company with a tax position that was challenged by the tax authorities (emphasis added):

“The payment of the assessment does not directly impact the recognition and measurement of the uncertain tax position. The uncertain tax position should continue to be assessed at the balance sheet date as if the payment had not been made. If the payment meets the netting requirements under ASC 210-20-45-1, it could be presented net against the UTP. If the payment exceeds the amount of the UTP, any excess would be recorded as a net tax receivable.”

A recent working paper by Bauer and Klassen, "A Comparison of Quantitative and Qualitative Disclosures of Tax Settlements to Assess Their Favorability," examines the odds of a favorable tax settlement for UTP.

According to the paper, their manual analysis of 800 tax footnotes identified that about 12% of the cases (97 observations) are settled unfavorably:

“We handcode 800 tax footnotes and classify the disclosure as consistent with a favorable settlement (238 observations), an unfavorable settlement (97 observations), or an inconclusive settlement (465 observations).”

Although, according to the paper, only a fraction of the cases are settled unfavorably, the Financial Times piece explains why losing those appeals could be significantly detrimental to the bottom line.

For example, in the quarter ending September 30, 2023, VF Corp had to reverse its roughly $900 million (including interest) tax receivable after losing the appeal:

“The clothing group VF Corp, which owns The North Face and Vans brands, paid the IRS $876mn in 2022 after losing a long-running tax court tussle over the accounting for its acquisition of shoe brand Timberland, but added the money back as an IOU on its balance sheet, on the basis it was likely to get it back after an appeal. Less than a year later, a US appeals court sided with the IRS and the one-sided IOU turned out to be worthless. It was written off in the 2024 accounts, dinging VF’s net income.”

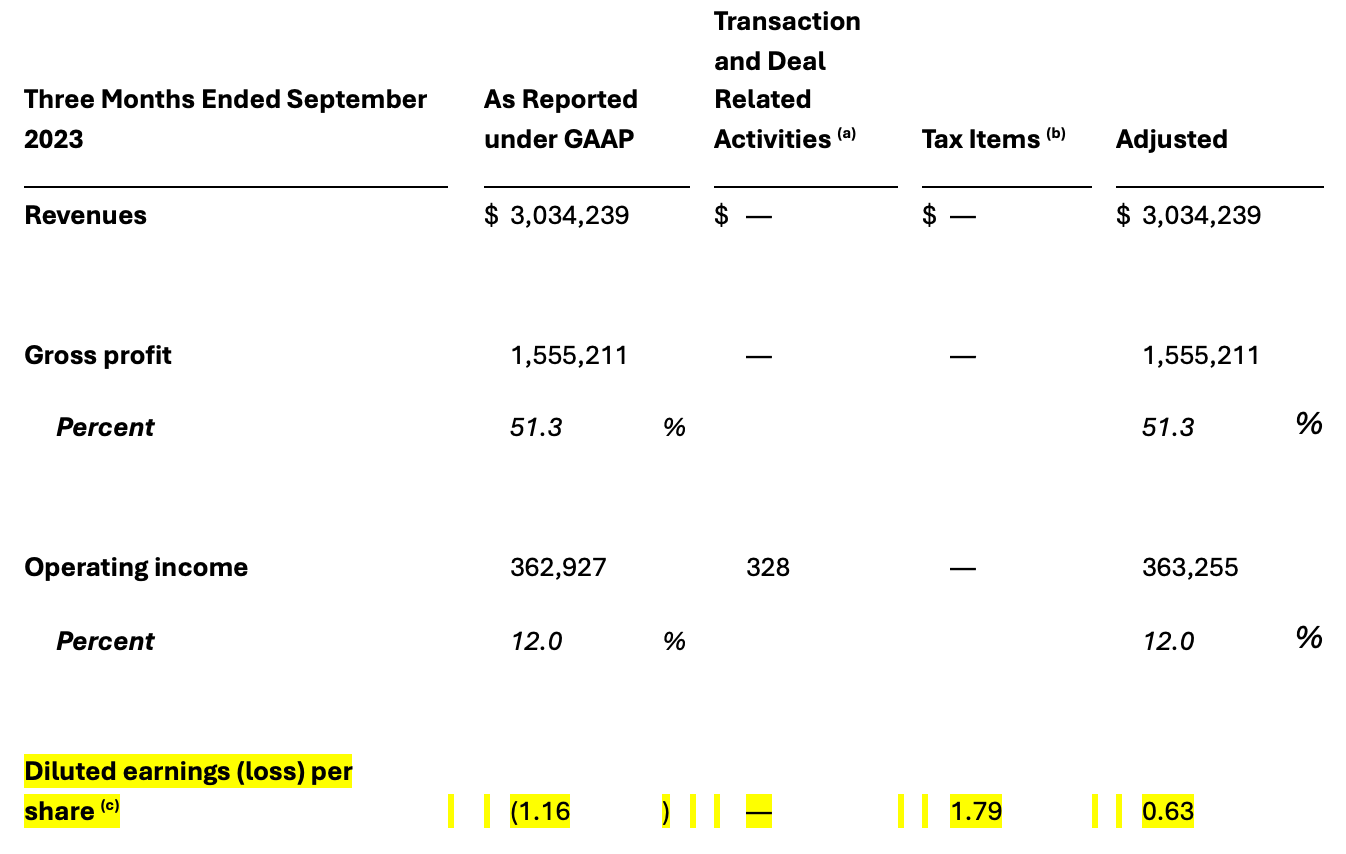

But what about non-GAAP? Surprising nobody, VF Corp removed the negative impact of the tax ruling in the Company’s non-GAAP presentation – effectively characterizing it as an unusual non-recurring charge. The adjustment for the cash payment plus accrued non-cash interest income turned the GAAP-basis diluted net loss of <$1.16> EPS for the quarter ended September 30, 2023, into a profit of $0.63 Adjusted EPS by adding back an equivalent of positive $1.79 in EPS.

Figure 1 – VF Corp non-GAAP presentation for the period ending September 30, 2023

Source: SEC filings

VF Corp had to explain the massive tax-related charge during its fiscal Q2 2024 earnings call. The good news? It could say that the tax court decision did not affect liquidity. Why? The cash payment was made the prior year (emphasis added):

“Q2 adjusted earnings per share was $0.63, down $0.10 versus fiscal 2023 largely due to elevated interest and tax, with higher tax driven by jurisdictional mix and the reversal of tax interest income that had been accrued associated with the Timberland tax payment. A quick comment on the reported tax expense in Q2. On September 8, the Appeals Court ruled in favor of the IRS in the Timberland tax case with regards to the timing of income inclusion from the Timberland acquisition in 2011. We're disappointed with the outcome and still believe in the technical merits of our case. This decision has no impact to our cash or debt outlook for fiscal 2024 as the payment was made last year, but we recognized a noncash $690 million net increase to our reported tax expense in Q2 which includes anticipated refunds of some tax payments for prior years.

The process of filing amended returns for each tax year across both federal and multiple state jurisdictions will take time, and we're not assuming any benefits to cash over the next 18 months from these refunds.”

However, the impact in liquidity was far from positive at the time of the payment in 2022, when VF Global was forced to sign a $1 billion term loan finance agreement to make the payment. From the transcript of the earnings release for the quarter ended December 31, 2022, available on VF Corp’s website:

“As it relates to our cash position at the end of Q3, as anticipated, our liquidity increased during the quarter to approximately $1.9 billion, benefiting from the seasonality of earnings and a reduction in working capital. Within the quarter, we paid the Timberland tax deposits of approximately $875 million, funded by the issuance of a $1 billion term loan, which will mature in December 2024.”

According to the Company’s 10-K filing, the term loan was issued in August 2022 and carried a weighted interest of 5.73% as of March 2023 – an equivalent of about $57 million additional annual cash interest expenses:

“Term Debt Facility

In August 2022, the Company entered into a delayed draw Term Loan Agreement (the “DDTL Agreement”). Under the DDTL Agreement, the lenders agreed to provide up to three separate delayed draw term loans (each, a "Delayed Draw”) to the Company in an aggregate principal amount of up to $1.0 billion (which may be increased to $1.1 billion subject to the terms and conditions of the DDTL Agreement). The DDTL Agreement has a termination date of December 14, 2024….

During the third quarter of Fiscal 2023, VF completed two draws under the DDTL Agreement totaling $1.0 billion, all of which will mature in December 2024. In connection with the draws, VF elected a base rate of one-month Term SOFR. The weighted average interest rate at March 2023 was 5.73%.”

This suggests a question for investors: How can investors identify companies that inflate non-current assets for years by reporting cash paid to tax authorities to appeal as a receivable? As we can see, sometimes those "assets" are funded by more debt.

Olga and I discussed in depth the ongoing $6 billion tax dispute between the Coca-Cola and IRS.

Coca-Cola Faces $16 Billion Tax Battle: Ongoing Dispute with IRS Puts Profit and Liquidity at Risk

Coca-Cola (Ticker: KO) issued a press release on August 2, 2024, just a few days after its 10-K filing, warning investors that the U.S. Tax Court took the next step in the ongoing tax dispute between Coca-Cola and the IRS. The court’s latest decision may cost the Company as much as $16 billion in back taxes. The dispute focuses on an alleged $9 billion …

After the paywall, we identify nine additional companies with tax dispute-related receivables that may be sitting on the books for years.

The table below outlines material tax disputes disclosed by US-based publicly traded companies, which classified the cash payments to facilitate an appeal as an asset on the balance sheet. The disputes involve international and domestic tax authorities and often concern complex issues such as transfer pricing, VAT treatment, and intercompany transactions. The disputes span a wide range of jurisdictions, tax years, and potential financial impacts.

Finally, we include a discussion of tax-related Critical Audit Matters (CAMs). According to the PCAOB, CAMs are audit-related matters that involve especially challenging, subjective, or complex audit judgments.