Stablecoins, Stollers, and shared auditors (again)

New timely work at Chicago Booth Review, the Stoller brothers are on fire, and recidivist lawbreakers Berkshire Hathaway and Union Pacific do some major moating.

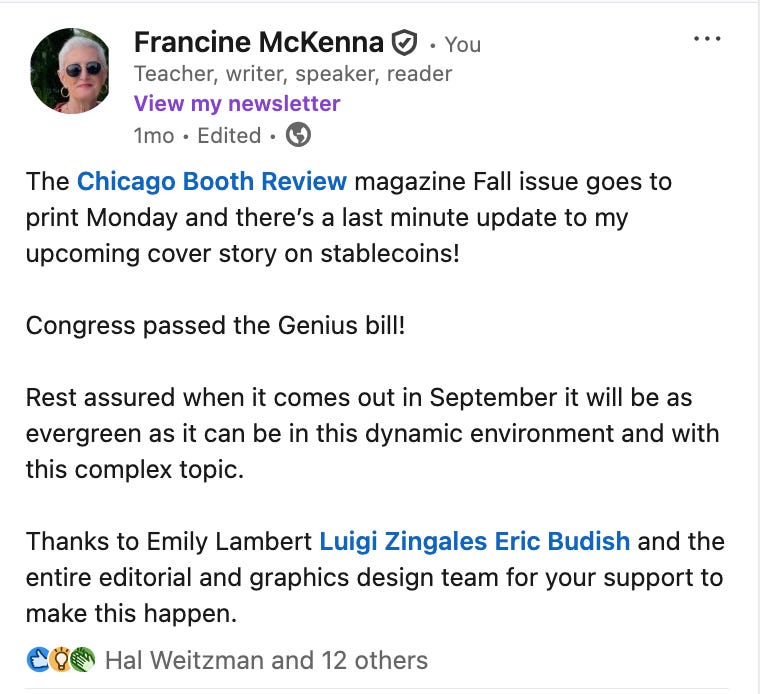

It’s live! My fall feature cover story for The University of Chicago Booth School of Business Review. So many sidebars!

I started working on this with Booth Review Deputy Editor Emily Lambert more than a year ago, early summer of 2024. As we all know, at that time the digital asset landscape was uncertain, unstable, still reeling from the FTX implosion and highly contentious under Biden's SEC Chair Gary Gensler. All that changed when Trump was re-elected President in November.

It's as if the Red Sea had parted and many could now see the vast treasure that had been previously unreachable under the swirling waters.

Over the next almost year I tried to put pen to paper, or rather fingers to keyboard, to establish a draft beachhead. Emily and I settled on an outline in early January and then, by the end of the month, I had a first draft. I had been reading and collecting articles, papers, and other material previously in a file folder on my hard drive.

But, there continued to be so much news, especially immediately after the January 20 inauguration, that the text was incredibly slippery. In late April, I interviewed Professors Luigi Zingales and Eric Budish, and reached out to other researchers cited in order to get the freshest possible take on their writings, interviews, and research.

Finally, a month ago today, just when we thought we had a final draft, one as evergreen as it could be for a fall print publication, the inevitable occurred:

I hope you like the article and the two sidebars — on crypto and classical monetary theory and one on crypto's big lobbying efforts — even though it has no accounting or audit content!

*****************************************************************************************************

I have been watching the Apple+ series The Studio and it's eerie for me to watch the prominent role played by writer/director Nick Stoller! That's because he is the brother of Matt Stoller, someone I have known for a long time, talk to off and on, and often cite as the author of the Big newsletter on antitrust and competition.

They have the same face, the same voice!

Matt the New Brandeisian, not Nick the comic banterer, has a couple of great blurbs in his Sunday Big Monopoly Roundup.

Warren Buffett is buying a big stake in UnitedHealth Group. America’s folksiest predator!

I guess it was a no-brainer that Berkshire Hathaway (audited by Deloitte since 1985) would buy some United Health (audited by Deloitte since 2002) shares. I get all the arguments that it is perhaps only temporarily undervalued but I suppose Deloitte would know for sure!

The Kingswell newsletter laid it all out:

There’s no question that United Health has been through the wringer of late — grappling with a devastating cyberattack, the tragic murder of CEO Brian Thompson, the subsequent (and sudden) resignation of his successor a few months ago, a Department of Justice investigation into alleged Medicare irregularities, and a downward revision to the current year outlook. With that parade of horribles in mind, it’s not too surprising that United Health’s stock price has fallen 46.2% so far this year.

But boy oh boy does Berkshire Hathaway's — and whomever is making these investment decisions — hypocrisy shine through.

What’s that famous Buffett quote?

It takes 20 years to build a reputation and five minutes to ruin it.

If you think about that, you’ll do things differently.

This one from Buffett about moats is more apropo:

The most important thing to me is figuring out how big a moat

there is around the business. What I love, of course, is a big castle and a

big moat with piranhas and crocodiles.

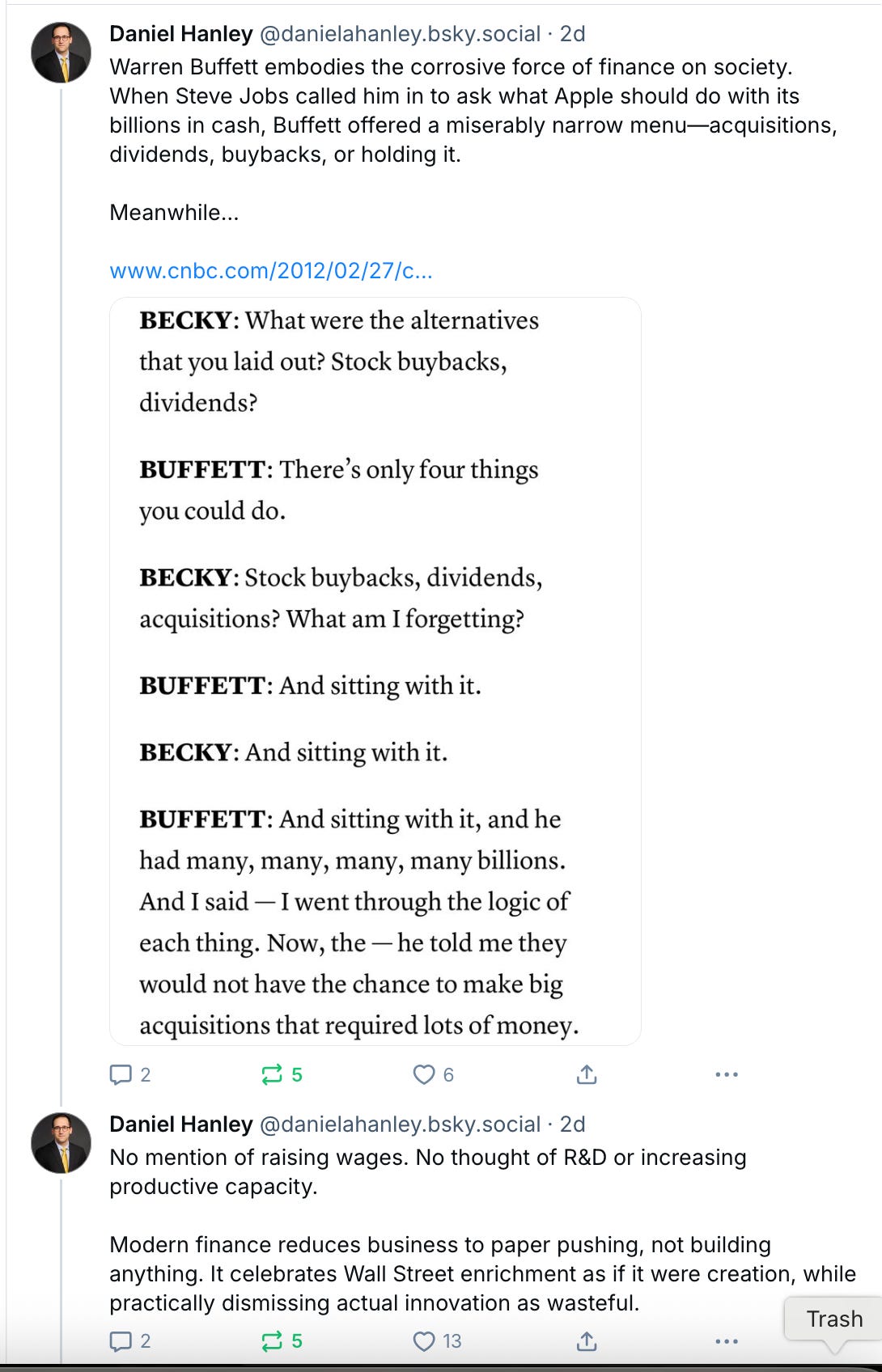

Here's Daniel Hanley, Senior Legal Analyst at Open Markets Institute, on BlueSky (Here's the CNBC link embedded in the post):

I sent him a response linking to my 2013 Chicago Booth Review article on Apple and buybacks.

Yes, I have been writing for the Chicago Booth Review for a long time!

United Health has certainly had more than its fifteen minutes of fame as Andy Warhol would say. More like non-stop infamy.

I am not the only one to think that.

In other Berkshire Hathaway (BRK) news, Matt Stoller tells us in this Sunday’s weekly roundup:

Union Pacific [fm note: Audited by Deloitte since 1967] is lobbying to get its merger with Norfolk Southern [fm note: Audited by KPMG since 1982] through the Surface Transportation Board process.

Why is this BRK news? Because this combo will create an even more formidable competitor to Berkshire’s BNSF and, perhaps, "force" BRK to make another pricey acquisition.

No less than Kingswell said so!

I don’t know enough about this to definitively declare it bad news for BNSF, but the aforementioned Union Pacific agreed to acquire Norfolk Southern for $85 billion. If approved, this mega-merger would create the first true transcontinental railroad in U.S. history. Union Pacific would no longer be slowed by handing long-distance cargo over to one of the Eastern carriers at Chicago — but, rather, can now deliver coast-to-coast on its own tracks.

And there seems to be unanimous consensus among industry observers that this would all but force BNSF to seek a similar deal with CSX [fm note: audited by EY since 1980]. (Yes, it seems entirely un-Berkshire-like to be “forced” into a high-priced acquisition based on the moves of a competitor, but I’m just sharing what others are saying.)

· Greggory Warren of Morningstar wrote that BNSF “can no longer afford to ignore CSX”. (Pre-Covid, Warren served on the analyst panel at Berkshire AGMs — which is probably a fair sign that Buffett considers him to be a sharp analyst.)

“With BNSF already trailing Union Pacific, its main competitor in the western U.S. market, the last thing it needs is to worsen its competitive position by not pursuing a transcontinental U.S. railroad footprint.” He added that time is very much of the essence and that “a bid for CSX in the $83 billion range would not be an issue” considering the size of Berkshire’s cash mountain.

· The editor-in-chief from Railway Track & Structures echoed these thoughts. “Everyone correctly assumes that if UP + NS is announced, then BNSF + CSX would follow soon,” he wrote. “Having one transcontinental railroad and two regional Class I’s would not make any sense. We have four Class I’s in the United States. If two become one, then the remaining two will also become one.”

BNSF has been struggling.

Coincidentally, or not, according to this study by risk management firm Protecht, which used data on corporate violations collected via the Good Jobs First Violation Tracker, Union Pacific has been the most fined company between 2020 and 2024. Warren Buffet’s Berkshire Hathaway has received the second highest number of fines. The multinational conglomerate has been fined 503 times between 2020 and 2024.

Of the top 10 most fined companies, Berkshire Hathaway has both the highest total cost of fines, and the highest average fine.

[Union Pacific] has been fined 697 times during the five year period analyzed, with nearly 200 more fines than the second placed company. 691 of the 697 fines were for railroad safety violations. Of the 10 most fined companies, Union Pacific’s average fine per violation is the lowest at $10k per fine.

Union Pacific has received three fines over $100k - a $266,581 fine for a railroad safety violation in 2020[1], and a further $133,650 for another railroad safety violation in 2021[2]. They were also fined $260,000 in 2020 for an employment discrimination case[3].

Their 503 fines have cost them over $1.3 billion in fines, with an average fine of $2.7 million. 26 of Berkshire Hathaway’s fines have been for over $1 million. 81% of the violations by companies under Berkshire Hathaway’s ownership were for safety related offenses, accounting for $731 million worth of fines.

CSX is in third place. CSX has been fined 438 times, with the total sum of those fines adding up to $5.8 million in losses for the freight railroad company.

Although 97% of their fines were for railroad safety violations, 27% of the cost was made up from four fines for workplace whistleblower retaliation. The most expensive of which set CSX back $667,740 in 2021, as punishment for firing two railroad workers in 2017 at a railyard in Waycross, Georgia, when they encountered and reported a blue flag that signaled their train could not move safely[4].

Three of the five most fined businesses are railroad companies, with Norfolk Southern ranking fifth. Norfolk Southern’s 377 corporate violations have cost them $916 million.

The Atlanta based rail transportation company has been on the wrong side of two huge fines, both issued in 2024. They agreed to a $600 million settlement of claims by those impacted by the 2023 train derailment and fire in East Palestine, Ohio that released toxic substances into the air[6], as well as $310 million settlement with the U.S. Department of Justice for the damage caused by the Feb. 3, 2023 train derailment in East Palestine, Ohio[7].

Protecht’s VP of Risk & Compliance, Jared Siddle, commented on the findings of the study:

Corporate fines aren’t just a cost of doing business, they’re signals of systemic risk and governance breakdowns. Our analysis reveals patterns of repeat violations that point to deeper operational and cultural issues. Companies that fail to embed risk awareness and accountability at every level ultimately expose themselves to reputational, financial, and legal fallout. Effective risk management isn’t about box-ticking, it’s about building integrity into the core of business operations.

The full dataset can be viewed here.

© Francine McKenna, The Digging Company LLC, 2025

These are my scattered thoughts concerning BRK buying UNH:

I am a retired physician. Mainly I invest now. I have 10 shares of BRK.B. Before the last annual meeting of BRK, which I didn't attend, I noticed that BRK's portfolio and mine were completely different in what we owned. In addition, neither BRK nor I owned much in the way of health care or health insurance stocks. BRK at the time owned some shares of DaVita. That was all, as I recall.

I always wondered why Buffett and BRK then didn't own some health care companies. These companies seem to be able to increase prices steadily, which is one thing he looks for.

Buffett has described the health care system as a "tapeworm." He also, along with Bezos and Dimon, tried to establish a health care company, Haven, to compete with available and more expensive health care options. Haven failed, or at least has ceased to exist.

I don't know whether Buffett, or Ted/Todd, bought the UNH shares. I asked Perplexity who it thought bought the shares. It said that $1.5 Billion is a small purchase for BRK. It guessed that Ted/Todd bought the shares.

Whoever bought the shares, I wondered if BRK got an exceptional deal. In other words, were the shares bought on the market, or outside the market, at a discount. A company like UNH might sell BRK the shares at a discount, for the PR value of having BRK as a shareholder.