“KPMG is revamping how its global workforce will use artificial intelligence through a new deal with Anthropic that aims to make its tax and consulting services faster-moving and more efficient.

The deal marks the first time San Francisco-based AI company Anthropic will integrate its Claude tools on a Big Four tax platform. Some firms have made deals to provide employees with access to AI tools on the side without altering their main global platforms around Anthropic or its competitor OpenAI.

KPMG’s global tax and legal services lead the firm’s growth, with a nearly 8% increase in revenue to $9.3 billion in 2025. That’s compared with 6% for audit and 3% for advisory…

Anthropic has announced deals with accounting firms like Deloitte—which is a sponsor of CFO Journal—and PricewaterhouseCoopers, to develop industry solutions, among other things."

So which firm is remaining that does not have a business alliance and marketing conflict and can sign Anthropic’s audits? I think you can figure that out. Process of elimination leads you to the answer unless Kurt Hohl gets his way and any firm can do anything. In this case his firm wins either way!

The Dig is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

We’ve used the process of elimination technique before to figure out which firm audits pre-IPO OpenAI.

Stay tuned for my deep DIG into auditor independence later this week and my review of this SEC’s effort to dismantle protections of what is supposed to be a “public watchdog”. The statement about the growth of tax services is very pertinent!

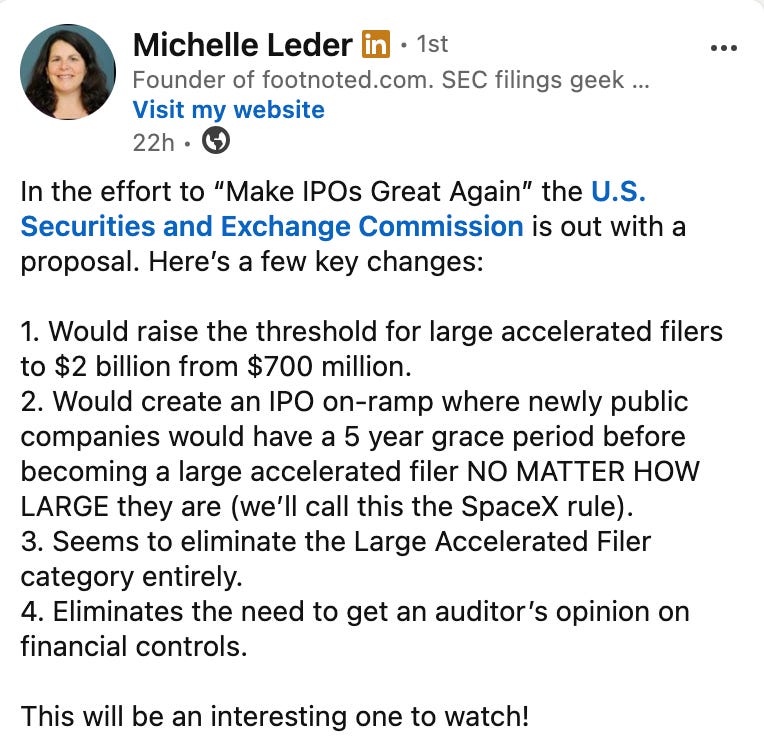

Footnoted.org’s Michelle Leder writes on LinkedIn:

I wrote: Raising the threshhold for large accelerated filers is backdoor way of eliminating more companies from required auditor internal control opinions. Used to have to pass legislation to water down SOx.

This from the press release basically tells the story of what they are up to :

"The proposed amendments would extend disclosure scaling and other accommodations currently utilized by smaller or emerging companies to approximately 81 percent of all current public companies. New public companies would enjoy these accommodations for a minimum of five years. The smallest public companies also would have additional time to file their annual and other periodic reports."

There is a lot more to say about this ridiculous and dangerous proposal, and I will do some data analysis of which Big 4 firms still do any SOX 404 work at all. You can bet on the fact that it now pales in comparison to tax and private equity work, and tax work for private equity.

In the meantime, take a look back at what happens when companies go public with chronic material weaknesses in internal control that don’t get fixed. And one firm in particular has repeatedly treated all its IPO’s like the citizens of Lake Wobegon, all of them are above average.

There’s a key quote towards the end of his Part 2 that is relevant to the SEC’s latest proposal to roll back SOx, in particular SOX 404 auditor opinions on internal controls.

The benefits include broader investor access, broader participation in economic growth, and dispersion of information through public markets.

The costs include greater exposure to financial downside, particularly if relaxing standards invites weaker or riskier firms into public markets. The costs also include the real expense of maintaining the scaffolding necessary for public companies to function properly: governance structures, internal controls, compliance systems, and enforcement.

If incentives for public listing increase, enforcement must also increase to counterbalance the greater risk of misconduct. Yet enforcement capacity itself has constraints. Regulatory agencies operate with limited staffing and resources. Expanding the public-company universe while reducing enforcement capacity would increase systemic risk. How does the desire for more public companies jive with the recent SEC enforcement staff cuts and PCAOB audit regulator budget and staff reductions?[23]

Reducing disclosure requirements or exempting more firms from internal control audits may lower costs on the margin. But it is not clear that these reductions would meaningfully change firms’ decisions to go public, especially when cheap private capital remains abundant. One of the primary benefits of staying private is the ability to retain control longer. If founders can grow their firms without subjecting themselves to analyst scrutiny, boards, and regulatory obligations, modest compliance savings may not shift that equilibrium.

If regulatory changes increase the number of public companies by a modest amount—say several hundred—those additional entrants will likely be the firms most sensitive to small cost reductions. That raises an important question: what are the characteristics of those marginal firms?

If such firms are highly cost-sensitive, they may also be more reluctant to invest in internal controls, governance, and compliance protections. Indeed, in my own research, I personally came across documented cases in which firms were willing to disclose material weaknesses in internal controls likely because hiring additional accounting personnel was deemed too costly. [24]

If such firms are highly cost-sensitive, they may also be more reluctant to invest in internal controls and basic financial reporting capacity. I remember one year reading every single material weakness disclosure submitted to the SEC, and some firms essentially said the same thing: they had a material weakness because they did not have sufficient accounting personnel, and it was “too costly” to hire more accountants. They treated that as an acceptable risk: disclosing a material weakness does not necessarily mean there is already a misstatement or a restatement; it means they are acknowledging that the risk of producing bad accounting is higher, but they are not willing to incur the cost now.[25] And we know that firms in that position are precisely the ones that often end up with restatements later.

In that sense, the cost is paid either now—through stronger controls and staffing—or later, when shareholders absorb the consequences through stock declines. The question is not whether the cost exists, but when it is imposed and who ultimately bears it.

Such disclosures do not immediately imply restatements, but evidence shows that firms with material weaknesses are more likely to experience reporting problems later. The cost is borne either upfront, through stronger controls, or later, through investor losses.

In that sense, shifting costs forward or backward does not eliminate them. It reallocates them to the near future.

Maybe the Big 4 don’t want to do audit anymore! Maybe SOX 404 is just an irritant with their clients, even the largest ones. Non-stop focus on advisory and tax and strong deemphasis on audit, with the planned replacement of auditors with AI, sure makes me think so!

In other news of dangerous moves on the enforcement front:

Financial Times, Kaye Wiggins in New York MAY 14 2026

“Wall Street’s top prosecutors want lawbreaking companies to hand themselves in, offering behind-closed-door deals that let them avoid being charged, fined or having full details of their fraud made public. The lenient new deals are available even in cases where alleged fraud was pervasive, caused severe harm, involved senior leaders and had already been reported in the press or by a whistleblower.

Prosecutors might charge individuals, but they would not charge companies even if the wrongdoing was worse than originally admitted. They would also not publish details of the deals.”

If there’s no fine and the deals are secret there’s no whistleblower bounty.

If there’s no “public statement of fact” there’s no deterrence or information for shareholders or harmed consumers to use to know if they were cheated and should be reimbursed.

It’s the kind of program you use for criminal corporations and their executives after a fascist takeover to provide them amnesty from providing material support for crimes against humanity.

I was quoted a couple of weeks ago about the SEC’s terrible proposal to make quarterly reporting optional.

CFODive

SEC unveils blueprint for ditching quarterly reporting

The proposal is part of the “Make IPOs Great Again” push aimed at reducing the “rigidity” of rules governing public companies, SEC Chair Paul Atkins said Tuesday. Published May 5, 2026 Maura Webber SadoviSenior Editor

Francine McKenna, an adjunct professor at Montclair State University in New Jersey and author of the substack accounting newsletter “The Dig,” said she was strongly opposed to the proposal, calling it a misguided attempt that addresses the quantity rather than the quality issue that is already affecting financial reporting.

Many companies put out financial reports with non-standard non-GAAP numbers in earnings releases and conference calls, and the less frequent filings will mean investors will need to wait longer to get more clarity on what is going on at a given company.

“The emphasis on alternative and non-GAAP metrics is only going to increase,” McKenna said in an interview.

I have had other cause to read a lot of Enron material recently. I will leave you with this comment, one that came right after the implosion, before even Arthur Andersen disappeared. (This guy thought Paul Volcker could pull it out…)

This was written by Robert Litan in April 2002, for the Brookings Institution. It is incredible that some want to go backward, implying companies don’t have the means 24 years later to report more frequently and accurately and not less so.

Using the Internet, many companies now or may soon have the ability to make their financial reports available to the public much more frequently than once a quarter. Indeed, financial institutions typically balance their books every night. Why not consider ways to have this financial information communicated to the public in the same time frame?

There will be objections to encouraging companies to make available frequent and unaudited financial information, but these objections can be met. Currently, quarterly financial data are unaudited and will remain that way unless the SEC or a new PRB come up with guidelines for more limited audits of data that is more frequently reported. In any event, the capital markets would become much more volatile if investors came to believe that all unaudited financial information was useless.

There is an even more compelling case for more frequent financial disclosures. Former SEC Chairman Arthur Levitt was one of the first to sound the alarm about the seemingly uncontrollable trend toward earnings management-or the manipulation of quarterly earnings reports to achieve or exceed market expectations, which is evidenced by the significant increase in earnings restatements over the past few years. If, however, companies routinely reported their financial results more frequently than every quarter, it is conceivable that investors and analysts would lose interest in the quarterly figures. Furthermore, it is highly doubtful that analysts would take the trouble to develop earnings forecasts more frequently than on a quarterly basis. Thus, there is a real chance that more frequent reporting could end incentives of managers-and their auditors-to engage in earnings management. The challenge is to find a way to provide incentives to the firms that are able to report more frequently than quarterly to do so.